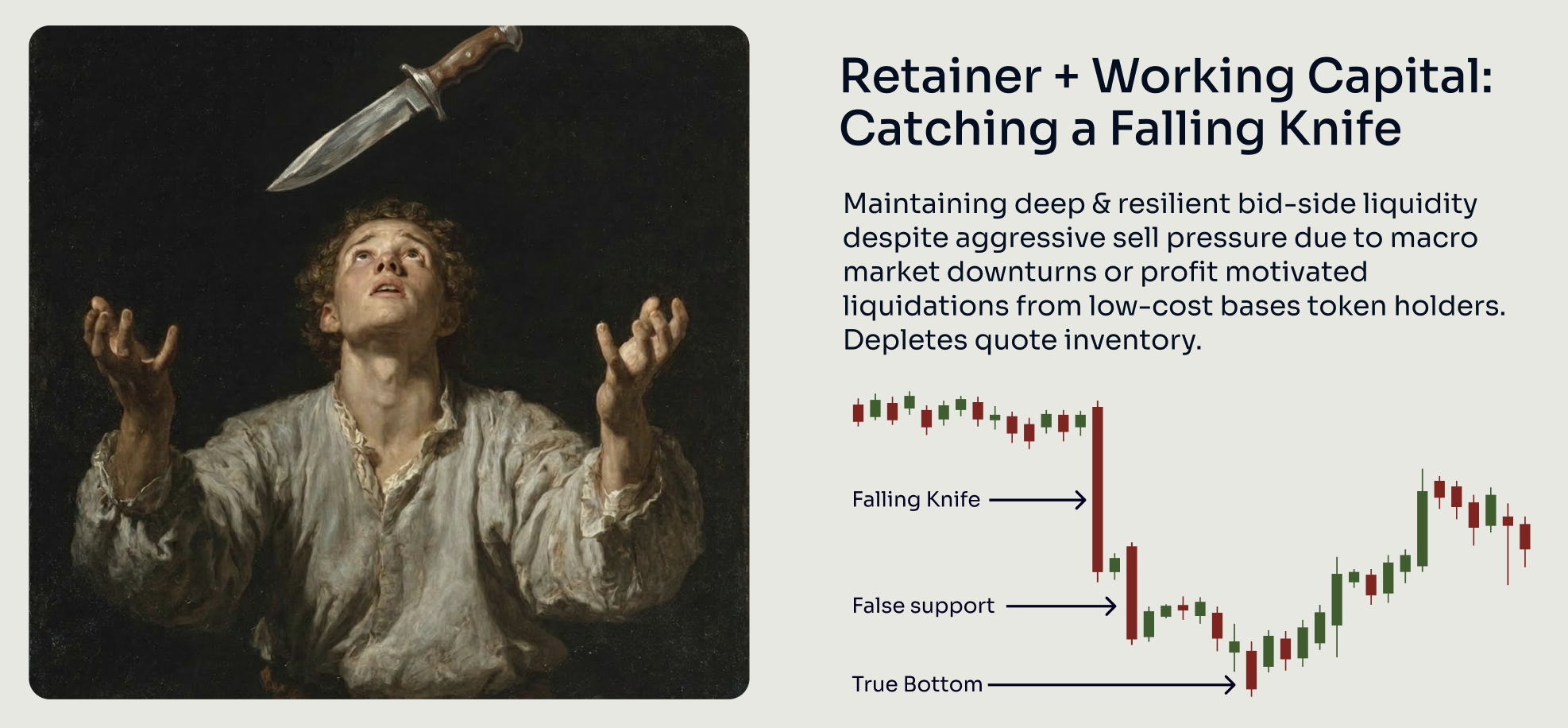

"Catching a falling knife" describes the structural risk inherent in retainer + working capital engagements during sustained market drawdowns. Because the market maker is obligated to maintain two-sided liquidity — placing both bids and asks — they must continue buying tokens even as the price declines. This converts their stablecoin working capital into depreciating token inventory, creating dangerous portfolio skew.

Consider a simplified example: a market maker begins with a balanced inventory of $1M in tokens and $500K in USDT, totaling $1.5M in notional value. As the token price enters a steep decline, the market maker's bid-side orders continuously fill — absorbing sell pressure from retail participants, insiders, and other market participants looking to exit. With each fill, the market maker's stablecoin reserves shrink while their token holdings increase.

If the drawdown continues — say a 70% decline from peak — the market maker may attempt to rebalance by selling some accumulated tokens, but this only accelerates the price decline. Meanwhile, the tokens they absorbed at higher prices are now worth a fraction of their purchase cost. In the example scenario, the portfolio that began at $1.5M could be reduced to roughly $390K in total value: the stablecoins largely depleted and the remaining token inventory severely devalued.

This dynamic illustrates the fundamental risk of the retainer model: it is the project's stablecoin treasury that bears the cost of providing liquidity during adverse market conditions. The market maker is effectively being paid to absorb losses that would otherwise be distributed across organic market participants. This is why retainer engagements carry meaningful risk to the project's working capital, particularly during prolonged bear markets or when the token lacks sufficient organic demand to support its price.