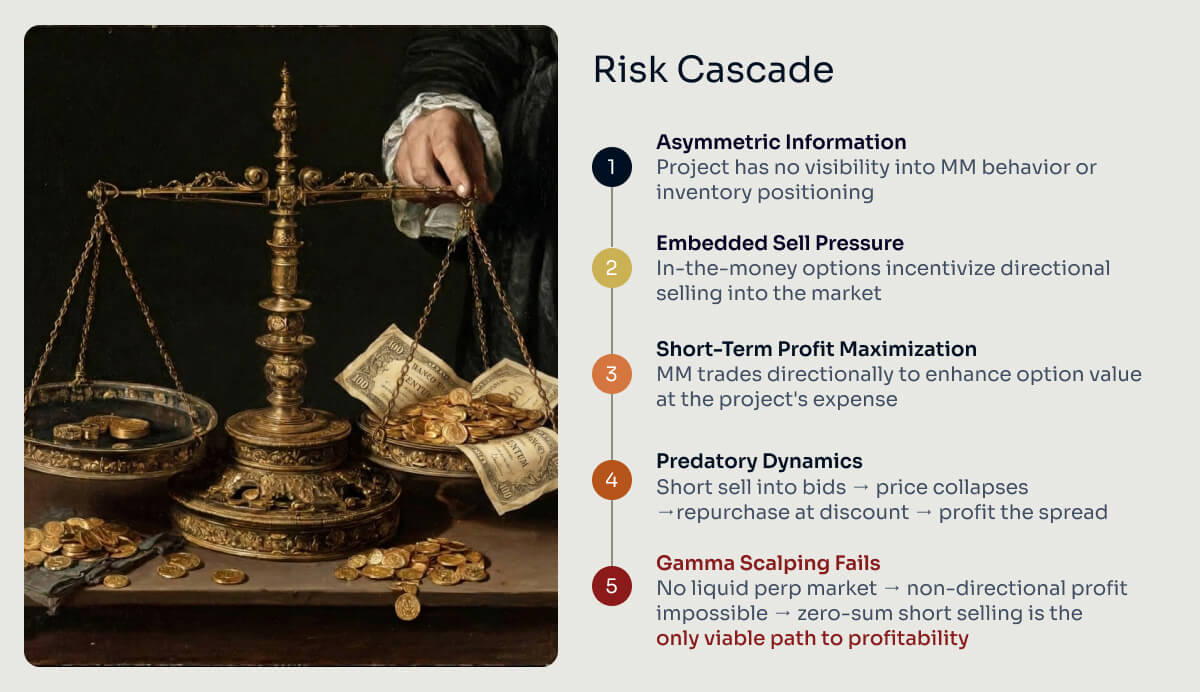

- Embedded sell pressure: Options that are deeply in-the-money create economic incentives for the market maker to monetize supply, which can translate into directional selling.

- Short-term profit maximization: Market makers may trade directionally to enhance option value, particularly around volatile events.

- Asymmetric information: Projects often lack visibility into the market maker's trading behavior, hedging activity, and inventory positioning.

- Predatory dynamics if poorly structured: Unrealistic strikes or large token allocations can incentivize post-TGE volatility harvesting rather than genuine liquidity provision. In the worst case, the market maker short sells aggressively into organic bid-side liquidity at elevated post-TGE valuations, drives down-only price action, and repurchases tokens at heavily suppressed prices to cover and return the loan — profiting the spread without ever exercising the option.

- Gamma scalping dependency: Gamma scalping is only profitable when a liquid perpetual futures market exists and the token experiences meaningful volatility around strike prices. For "down only" token launches or tokens without mature derivatives markets, the market maker has no viable non-directional profit strategy — leaving self-interested, zero-sum trading (short selling and covering) as the primary path to profitability.