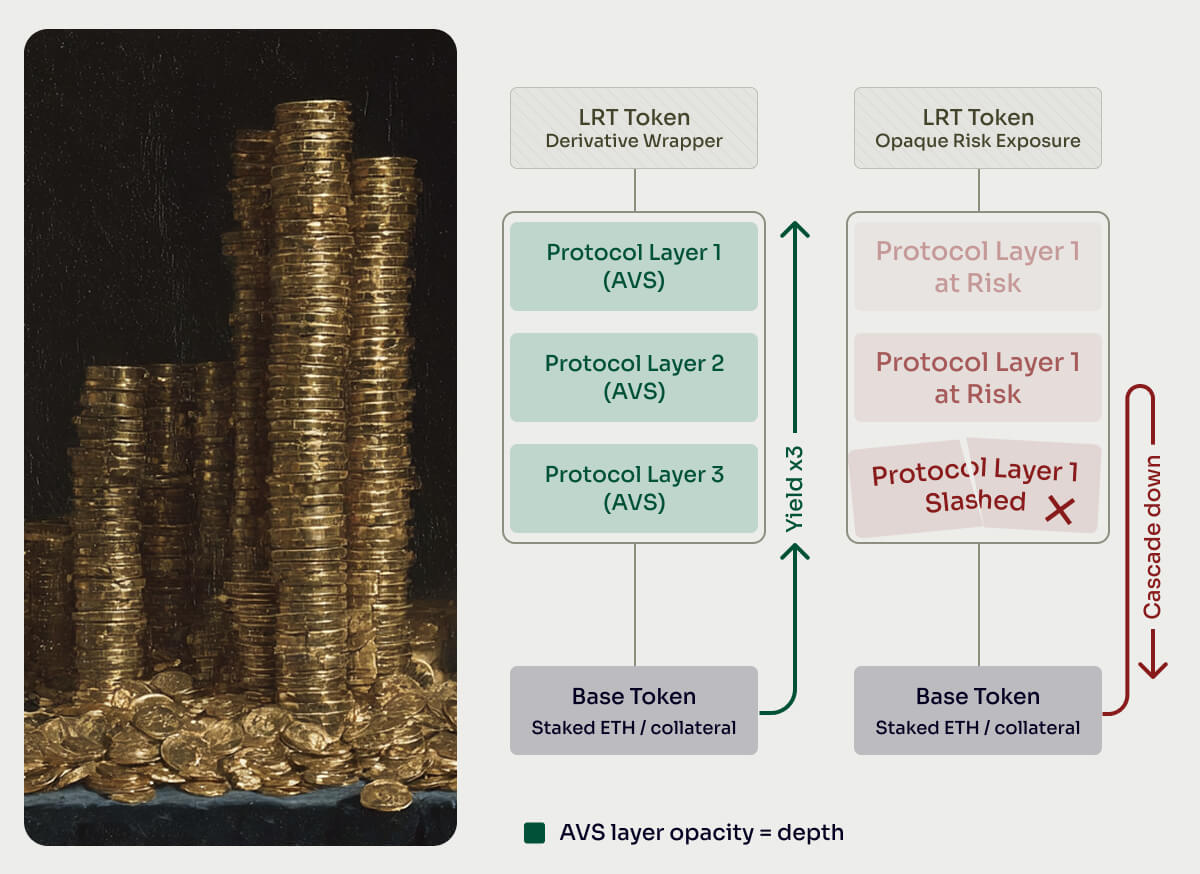

Restaking allows users to take tokens already staked on one network and simultaneously use them as security collateral for additional protocols or services. The concept was popularized on Ethereum, where staked ETH can secure auxiliary services (called Actively Validated Services) without those services needing to bootstrap independent validator sets. In traditional staking, staked tokens secure one network and earn one yield source. Restaking extends this by pledging the same capital to secure multiple services simultaneously, earning staking yields from each. The staker opts into additional slashing conditions in exchange for additional rewards. Liquid Restaking Tokens (LRTs) add another layer, derivative tokens representing restaked positions that are tradeable and composable within DeFi.

Benefits: Capital efficiency improves as the same tokens earn multiple yield streams. New protocols can leverage existing validator infrastructure rather than building security from scratch. Restaking creates an additional reason to acquire the base token, supporting demand. And a shared security layer enables rapid deployment of new services that inherit the trust properties of the base network.

Risks: Restaking is effectively leverage, the same collateral secures multiple obligations. If a validator misbehaves on any secured service, slashing can cascade across all of them simultaneously. In stress scenarios (mass slashing, protocol exploits), collateral may be insufficient to cover all claims. Users opting in through LRT wrappers may not fully understand the slashing conditions they're accepting. And if restaking yields are primarily funded by token emissions rather than organic revenue from the secured services, the yield is reflexive and will compress over time.

From a tokenomics perspective, restaking is a variant of the Collateralization demand driver. The key evaluation question is whether additional yield justifies additional slashing risk, and whether that yield is organic or reflexive.