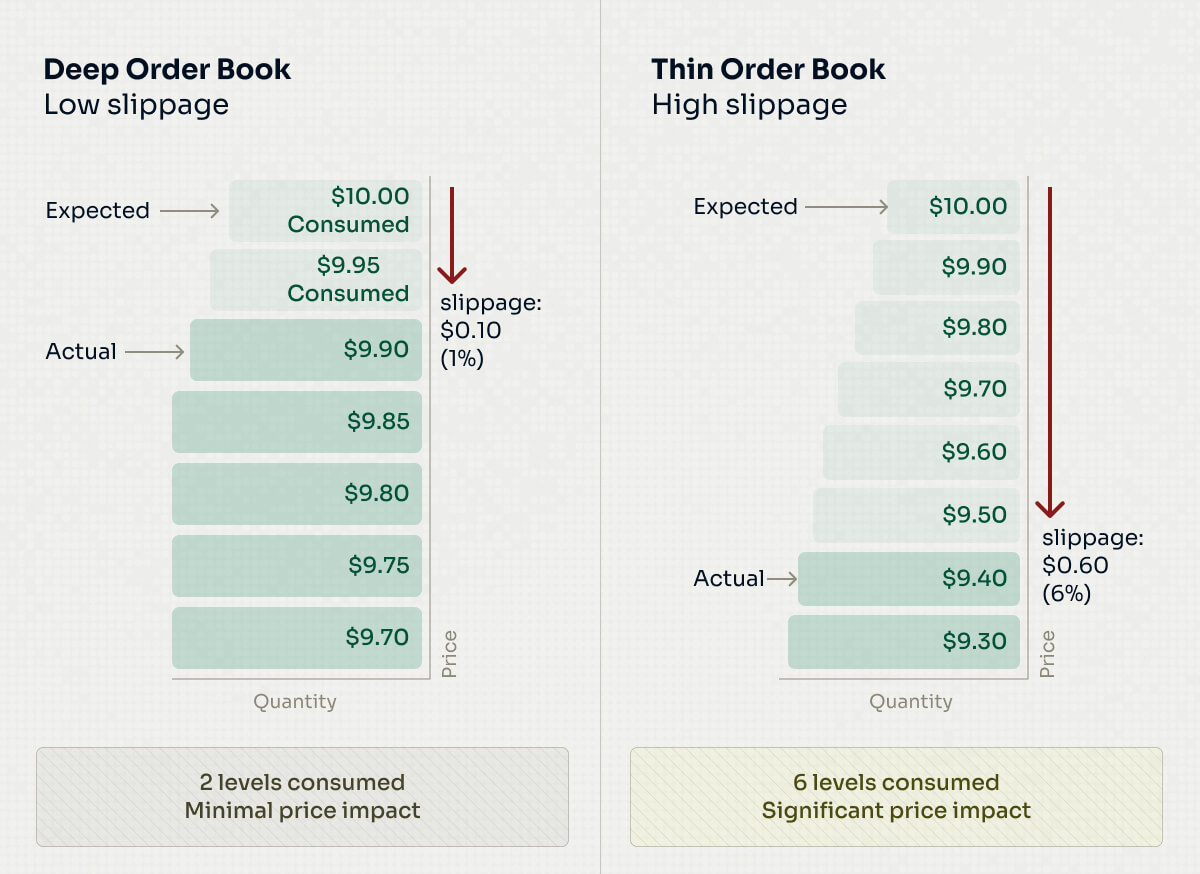

Slippage is the difference between the price a trader expects to execute at and the price actually received.

It occurs when order book depth is insufficient to absorb the full size of a trade at the quoted level. As an order consumes available liquidity, it moves through multiple price levels, resulting in a worse average execution price.

Higher slippage signals thin liquidity and increases transaction costs for participants. Lower slippage reflects deeper books and stronger market quality.